The Social Security Administration reports:

…over 1 in 4 of today’s 20 year-olds will become disabled before reaching age 67.

Those are some pretty rough odds! Given the risk, a disability policy can be a useful tool for protecting one’s income stream. If you decide to insure your future income by electing disability insurance, consider these four facets when selecting your policy.

Own Occupation

Table of Contents

“Own Occ” is the insurance industry’s jargon – it means “own occupation.” Electing a disability insurance policy that includes an “own occ” definition means the difference between:

-

-

- receiving disability benefit payments because your injury/illness prevents you from performing your regular job OR,

-

-

-

- not receiving disability benefit payments because – though you are disabled – you are still able to perform any job. This is called the “any occupation definition.” Consider an example:

-

In the course of his employment duties, Alexander the Great suffered a heady injury at the Battle of Granicus River. Due to the injury, Alexander is no longer able to comfortably wear his battle helmet. In this scenario, Alexander can no longer perform his “own occupation” of conquering large swaths of the crumbling Persian Empire.

However, Alexander’s head injury does not prevent him from performing other tasks – such as emptying out the chamber pots of the king’s personal bodyguard. This second job, however, does not pay as well as Alexander’s “own occupation.”

The above example illustrates the importance of electing a long-term disability (LTD) policy with an “own occupation” definition. Many LTD policies offer a temporal “own occupation” definition – switching from the “own occupation” definition to an “any occupation” definition after two years. This is especially the case with employer-provided disability plans.

Cost of Living Adjustment

COLA is the abbreviation for cost-of-living-adjustment. A COLA provides for an increase in benefit payments given inflation. This is critical because $3,000 today is not the same as $3,000 ten years from today.

Partial Disability

A LTD policy with a partial disability provision allows for benefit payments in the event that the insured can do some work, sometimes. For any balance of work that the insured disabled person cannot perform, the insurer will pay out a portion of disability benefits. Consider the example:

Alexander has partially recovered from his head injury. He is now able to wear his Macedonian Battle Helm for four hours each day. After that, Alexander must take a long nap – facilitated by several cups of wine.

If Alexander elected a LTD policy without a partially disability provision, he would receive no benefit payments in the previous scenario (above): in the event that he is partially disabled. Without a partial disability provision, benefits would only be paid in the event of total disability. With a partial disability provision, a LTD policy will pay out benefits in the event that the insured can only work on a part-time basis.

Elimination Period

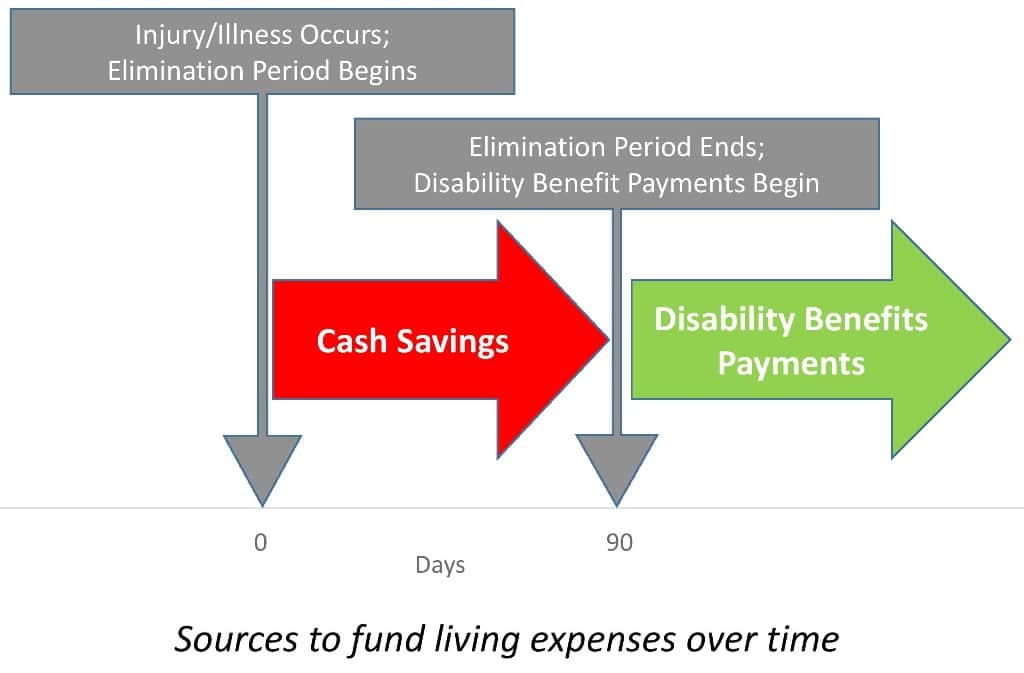

The elimination period is the waiting period before disability benefits are paid out. Common elimination periods are three, six and 12 months. The shorter elimination period, the higher the LTD policy premium. Electing a LTD policy with a longer elimination period can help manage the expense of insurance. However, the elimination period should be carefully considered. It is important that one’s cash savings be sufficient to float an individual through their elimination period.

If you’re only a couple years away from retirement, the need for disability insurance may not apply to you. With a sizable nest egg in place, any disability can be addressed by simply retiring early. A disability policy is most appropriate for younger individuals – those with years of earning potential yet to be realized.

If you’re unsure of how to decipher your existing employer-provided LTD policy – or are in the market for a LTD policy – work with a fee-only financial planner to help you navigate the important variables that affect how you will receive benefits in the event of disability.

Read: What to Look for in a Disability Policy, Part II

References

Social Security Administration. (2014). Official Social Security Website. Retrieved from Fact Sheet: Social Security: http://www.ssa.gov/news/press/factsheets/basicfact-alt.pdf